“Without change there is no innovation, creativity, or incentive for improvement. Those who initiate change will have a better opportunity to manage the change that is inevitable.”

– William Pollard, American Physicist

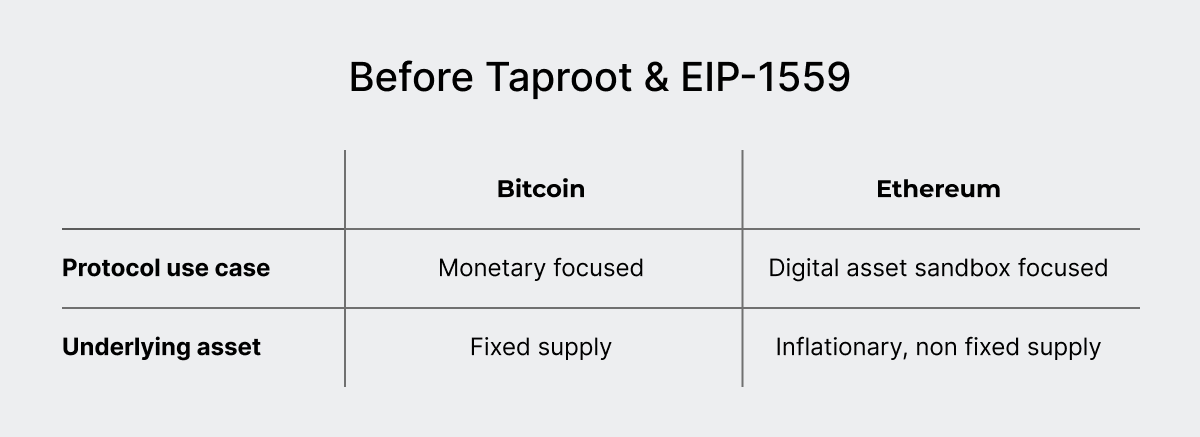

Throughout Bitcoin’s history, design choices have steered the protocol toward discouraging non-monetary activity. NFTs existed on the Bitcoin mainchain before the hype of NFT 2021, but they were challenging to mint and trade and thus uncommon. The inability to easily create unique assets and complicated smart contracts on bitcoin led to the arrival of Ethereum as we know it today, where individuals with minimal coding skills can issue unique digital assets on a public ledger. Bitcoin and Ethereum remained distinctive for many years (see image 1). However, due to the onset of ordinals, that has completely changed.

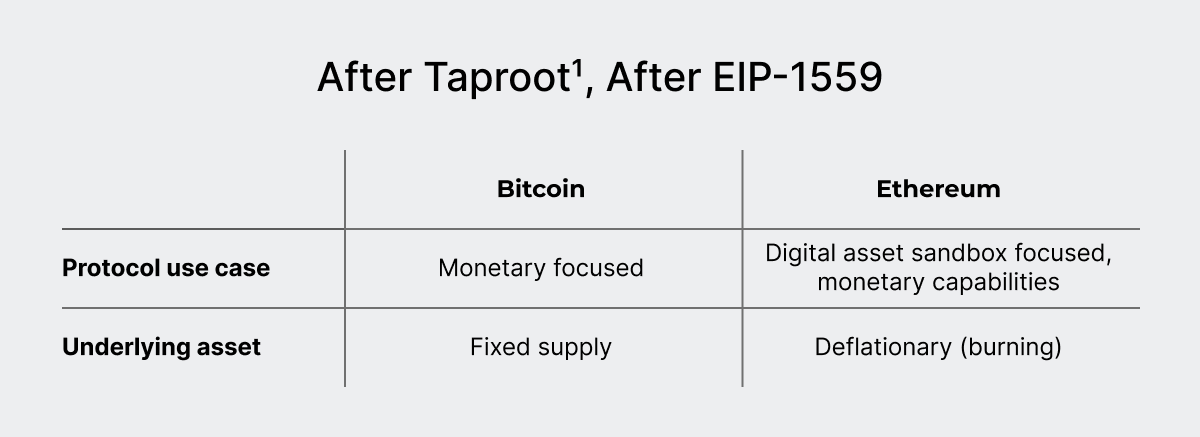

In 2021, the Ethereum protocol underwent a fundamental change, EIP-1559, to its transaction fee model. As a result, Ethereum’s underlying token, Ether (ETH), pivoted from being inflationary to essentially being deflationary. Thus, Ethereum and ETH can boast about its supposed monetary hardening.

Around the same time, Bitcoin underwent the Taproot upgrade (see image 2), squeezing in a few enhancements that initially seemed a little underwhelming. Since every major exchange at this time adopted segwit, bitcoin transaction fees were low. Without a sudden relief in high fees to validate Taproot’s arrival, 2022 saw little to prove people were utilizing the upgrade’s new features.

The excitement for 2023 began off-chain. Aside from a few prolific cryptocurrency exchange implosions, on-chain activity across Bitcoin and Ethereum remained business as usual. Nothing interesting to see here-

What’s that?

Someone figured out an easy way to create NFTs on bitcoin?

They are called Ordinals and they are easily tradable too?

And it’s not just NFTs but people are easily issuing tokens (BRC-20) on Bitcoin’s main chain?

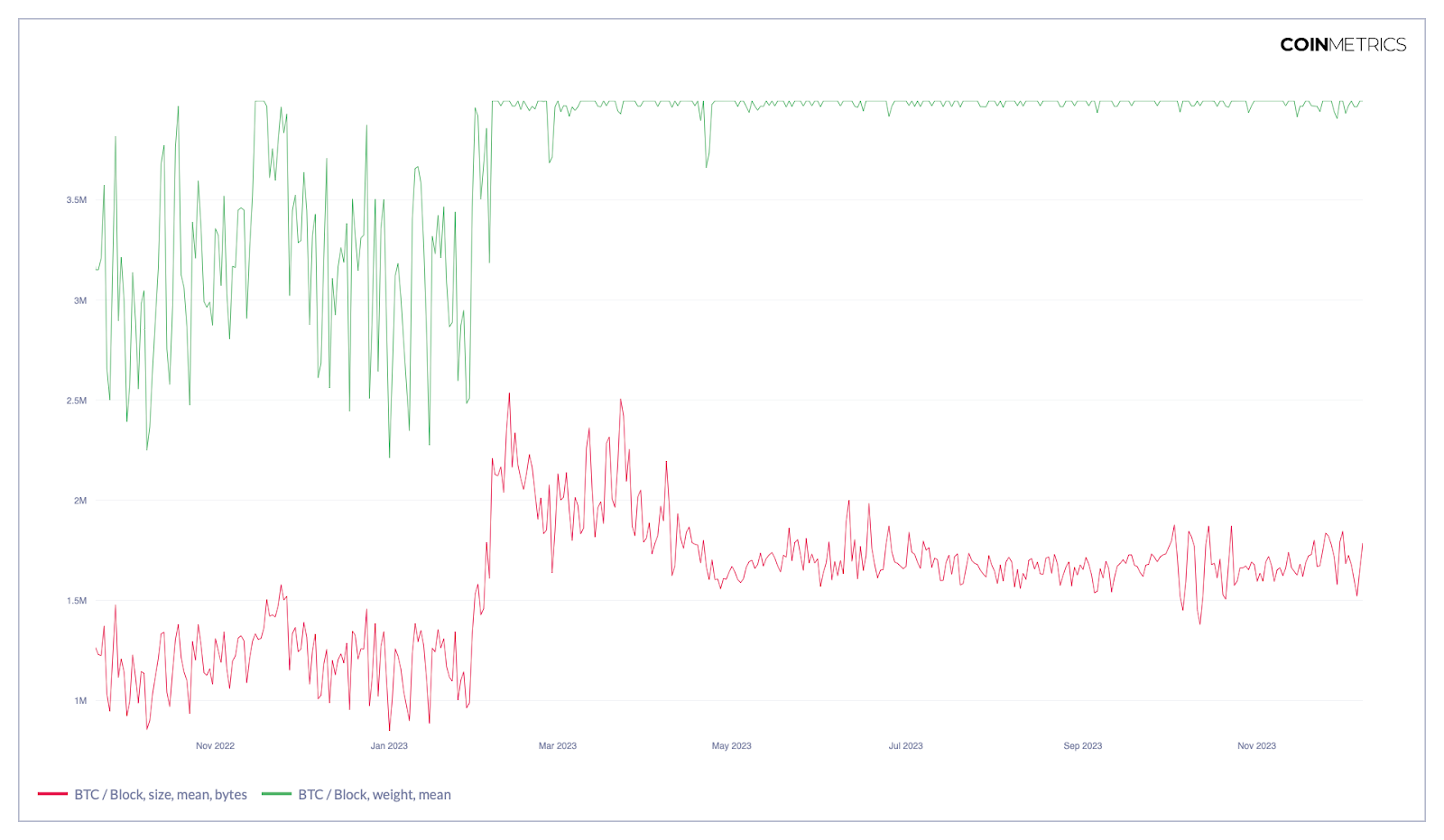

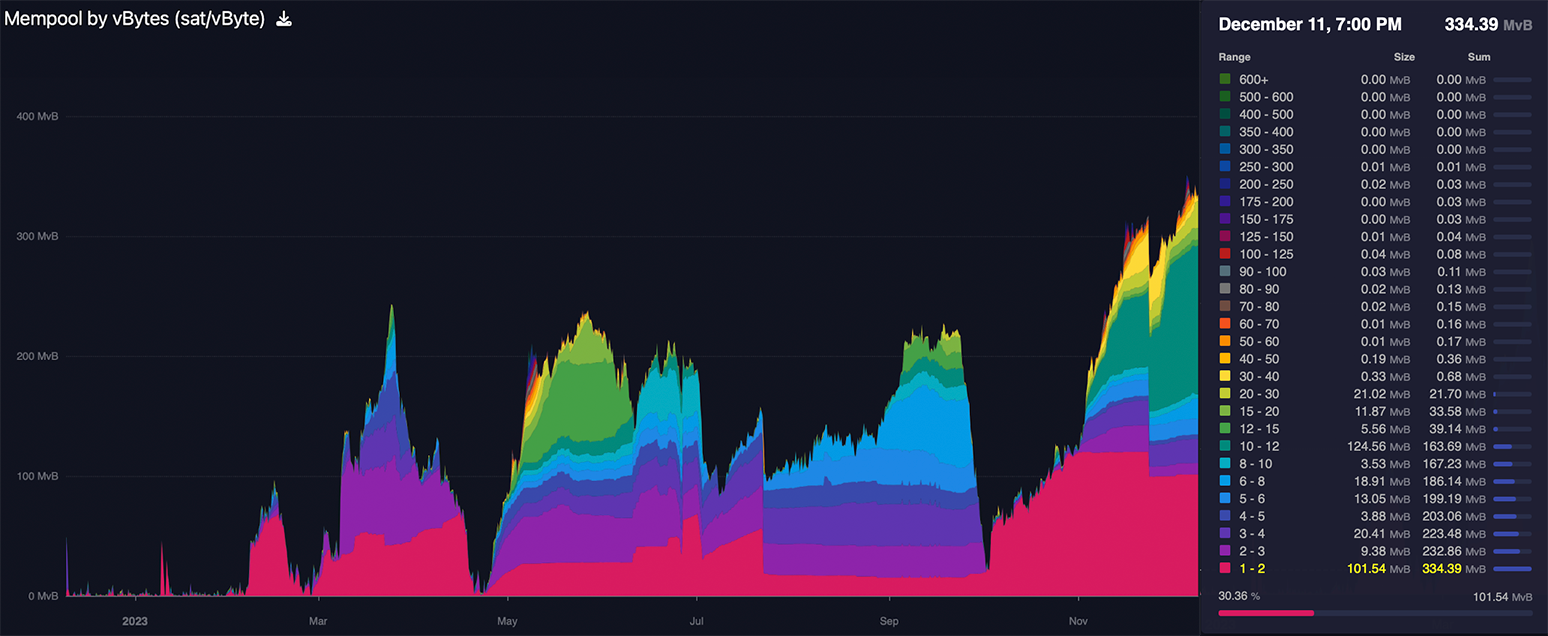

So, about a year and a half after Taproot’s release, the Bitcoin community figured out an easy way to issue customizable digital assets on the main chain. As a result, transaction fees are increasing, blocks are filling up (see image 3), and the mempool is packed.

While this is terrific news for Bitcoin miners and BTC holders, it’s less than great news for Ethereum stakers. The Taproot upgrade arguably diminishes the unique value propositions of Ethereum and other digital asset issuance chains.

As of late 2023, Bitcoin blocks are filled to the brim, regularly approaching their 4-byte theoretical maximum. Despite Bitcoin’s higher fees, users continue to issue digital assets on the network’s mainchain.

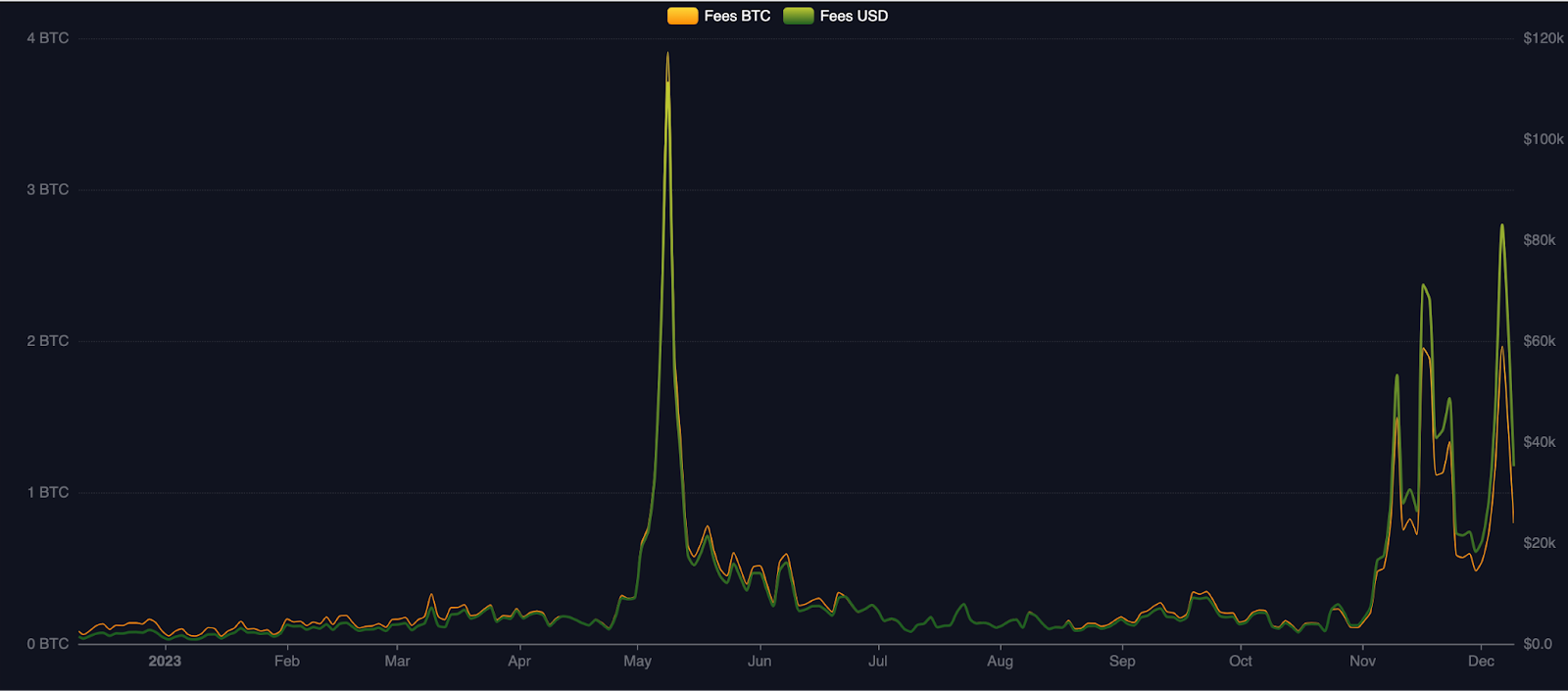

However, not everyone is pleased. Some bitcoiners want to censor ordinals and BRC-20s as they believe bitcoin ought to solely facilitate monetary transactions. Who is right? Should bitcoiners band together to censor ordinals because fees (see image 4) are becoming expensive ?

Did bitcoiners become too comfortable with a recently upgraded and underutilized blockchain? Did bitcoiners become too accustomed to the low main chain fees that accompanied it? Today, Bitcoin is confronted with a surge in block space demand – making use of excess block space (excess supply) – thus, every interaction with the blockchain is more expensive (see image 5).

As it becomes more useful, Bitcoin is becoming more expensive. This dynamic validates the concerns raised by the bitcoiners that wish to censor ordinals and restore bitcoin’s inexpensive monetary facilitation.

However, one could argue that even solely monetary bitcoiners ought to embrace Bitcoin’s expanded use case, as it will help drive Bitcoin innovation and adoption.

What happens if Bitcoin successfully demonstrates its ability to conduct unique asset issuance and interaction? Could the usage for all other blockchains dwindle?

As of mid December 2023, Bitcoin’s digital asset issuances do not appear to be cannibalizing transactions from other blockchains. These issuances serve as a form of community stress testing that, as of this article’s publication, has not seen Bitcoin compromise its decentralization or asset scarcity (see image 6). One could say the stress test is going well.

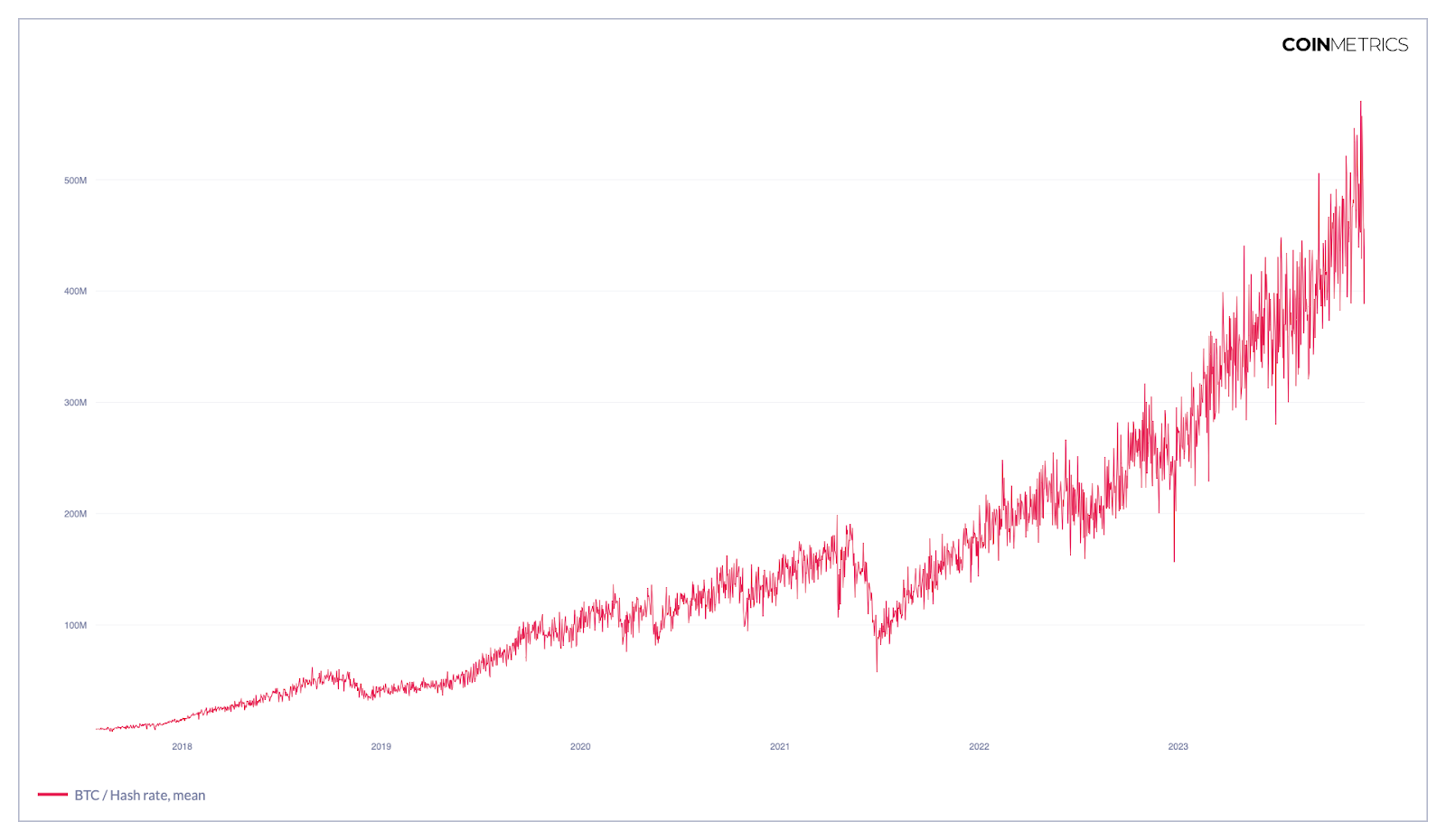

Bitcoin miners can perceive bitcoin’s new economic activity and accompanying higher fees as an increase to an already guaranteed stream of mining revenue that further incentivizes long term capital investments into the sector. If hashrate is any indication of potential future revenues, many miners seem to be on board (see image 7). Knowing that they will not have to drastically alter their operations in search of new revenue, Bitcoin miners pursuing long-term economic revenue can relax. Ethereum stakers may not enjoy that same comfort.

As Bitcoin grows and evolves, Bitcoin miners will continue to benefit from more fees without compromising any of the revenue stability that attracted them to this industry in the first place. What’s yet to be seen, however, is the impact that Bitcoin’s upgrades could have on other cryptocurrency projects? Will they take market share, attention and social capital away, potentially cannibalizing other ‘everything’ chains, or will the monetary only Bitcoiners win? What do you think?